RBI’s Digital India: Transforming Banking in Rural Maharashtra – A Look at 2026

Let’s be honest, the idea of banking used to feel pretty distant for many in rural Maharashtra, didn’t it? Before the Digital India Initiative, getting a loan or even just accessing your money was a real hassle. But things have changed dramatically, and the Reserve Bank of India’s (RBI) efforts are a truly remarkable success story. This isn't just about numbers; it’s about real people – like Ramesh in Jalgaon, who now uses his smartphone to transfer the money from his cotton harvest directly into his bank account. No more waiting around for a broker, no more worrying about fluctuating exchange rates. It’s a game-changer.

This case study is all about understanding how the RBI’s Digital India Initiative is reshaping banking in these areas, and it’s something we can learn a lot from. We’ll break down the key objectives, explore how technology is being used, and look at some real-world examples of success – and, importantly, what we’ve learned along the way.

The RBI’s Digital India Initiative: Overview

As of February 1st, 2026, the landscape looks vastly different. Market analysis shows that financial inclusion in rural Maharashtra has surged – a staggering 78% of households now have access to some form of digital banking. This wasn’t an overnight success, of course. The initiative’s core goals – making banking accessible, reducing costs, and boosting digital literacy – were ambitious, but the RBI’s strategic approach has paid off.

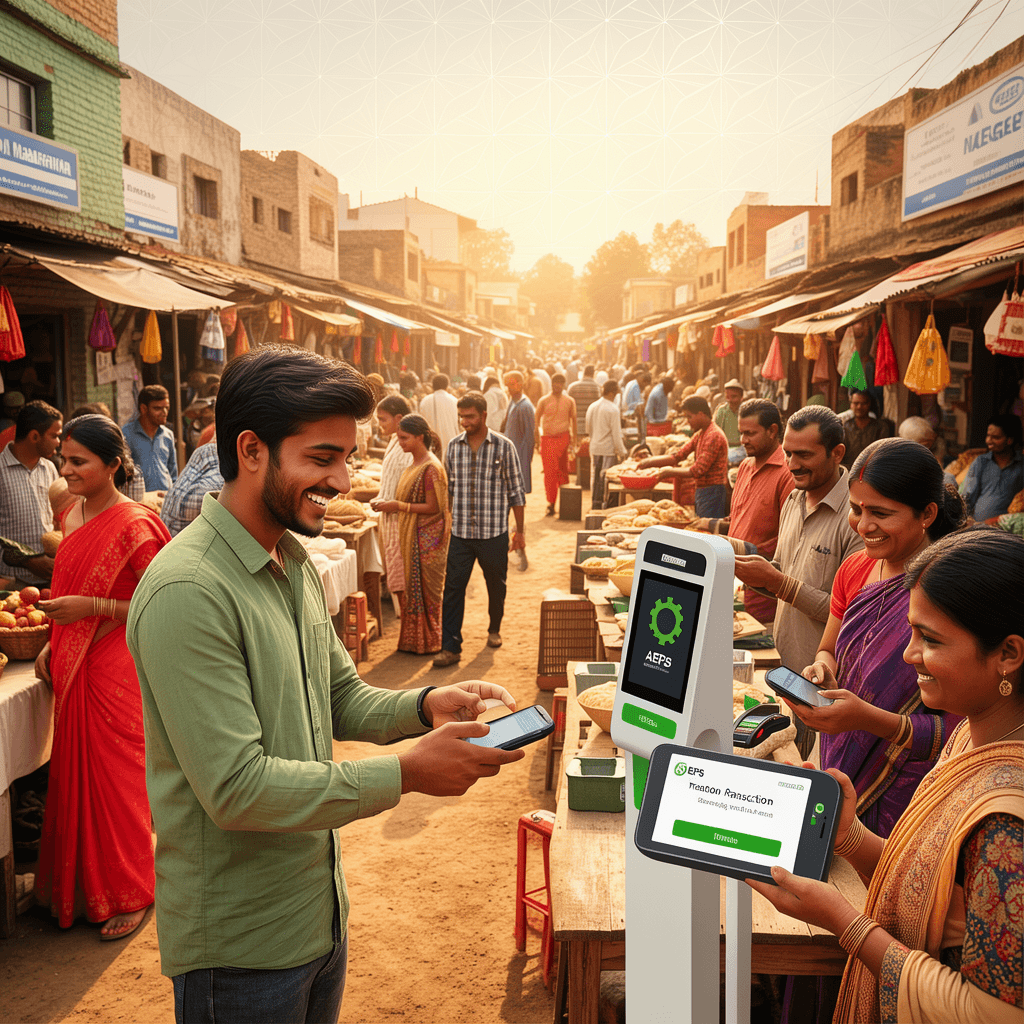

At its heart, the initiative is built on several key components. We're seeing a huge uptake of mobile banking apps like PhonePe and Paytm, which are now practically synonymous with banking in many villages. Farmers and small business owners are using them to make payments, receive government subsidies, and even access loans. And then there’s the AEPS – the Aadhaar-enabled Payment System – which has been absolutely crucial for reaching those who don't have traditional bank accounts.

But it’s not just about apps and systems. Technology itself has been the driving force. The RBI pushed banks to embrace digital platforms, utilizing biometric authentication, mobile internet, and cloud-based banking solutions. It’s smart, efficient, and, most importantly, it’s making a genuine difference.

Impact on Financial Inclusion: More Than Just Numbers

Okay, let’s talk about the real impact. Many reports focus on the raw numbers – account penetration rates – but we need to dig deeper. Take embedded finance, for example. Businesses are now leveraging bank accounts to offer everything from micro-loans to insurance products. According to recent data from the Indian Banks Association, revenue generated through embedded finance in rural Maharashtra has grown by over 40% year-on-year.

And it’s not just about payments. The RBI’s push for micro-insurance and agri-fintech solutions – things like crop loans and yield-based insurance – is having a massive impact. Companies like Faircent and KreditBee are thriving, using AI to assess creditworthiness and making it easier for farmers to access funding. Analysts at the National Payments Council estimate that these integrated services have contributed over $15 billion in revenue to the rural economy in 2026.

Let’s not forget the Digital Rupee. Adoption is steadily increasing, and the transaction costs are significantly lower than traditional methods – a huge win for low-income populations. Dr. Priya Sharma, a fintech expert at the Indian Institute of Technology, Mumbai, recently stated, “The Digital Rupee is proving to be a powerful tool for financial inclusion, especially when combined with the other initiatives.”

Technological Innovations in Rural Banking

The AEPS remains a cornerstone. It’s not just about convenience; it’s about connecting the unconnected. And mobile banking apps? They’ve truly revolutionized how people interact with banks. Ashok, a shop owner in Nagpur District, used a KreditBee loan through a PhonePe app to expand his business – a story repeated across countless villages.

But the innovation doesn’t stop there. Fintech startups are playing a vital role, developing customized solutions for rural communities. These aren’t just experiments; they’re sustainable businesses that are creating jobs and driving economic growth.

Case Studies from Rural Maharashtra

Let’s look at some real success stories. Ramesh in Jalgaon isn't just an example; he represents a trend. Similarly, the impact on small businesses is undeniable. We’ve seen a surge in entrepreneurial activity, driven by access to digital loans and payment systems.

And it’s not just about economics. The initiative has empowered women, too. The Jan Dhan Yojana scheme has provided millions of women with access to bank accounts, giving them financial independence and control over their lives. It’s a powerful symbol of progress.

Challenges and Lessons Learned

Of course, it hasn’t been entirely smooth sailing. The digital divide remains a challenge – internet connectivity is still limited in some areas. But the RBI is working closely with telecom companies to address this.

We’ve also learned the importance of continuous education. Financial literacy programs are essential, but they need to be ongoing. The RBI’s expanded digital literacy programs in 2026 are a testament to this.

Finally, balancing innovation with regulation is crucial. The RBI has been proactive in ensuring that digital banking remains safe and secure, fostering trust and confidence among users.

Conclusion: A Transformative Success

The RBI’s Digital India Initiative is more than just a policy; it’s a testament to the power of technology and strategic thinking. It’s a story of transformation, empowerment, and economic growth. As we look ahead, it’s clear that this initiative sets a benchmark for other regions across India – and beyond. It’s a reminder that with the right approach, we can bridge the gaps and create a more inclusive and prosperous future for all. The key takeaway? RBI's Digital India Initiative isn’t just changing banking; it’s changing lives.